Understanding Auto Loan Amortization

When you finance a vehicle, you agree to pay back the loan amount (principal) plus interest over a set period. While your monthly payment remains constant, the way that payment is applied changes with every single installment. This process is called amortization.

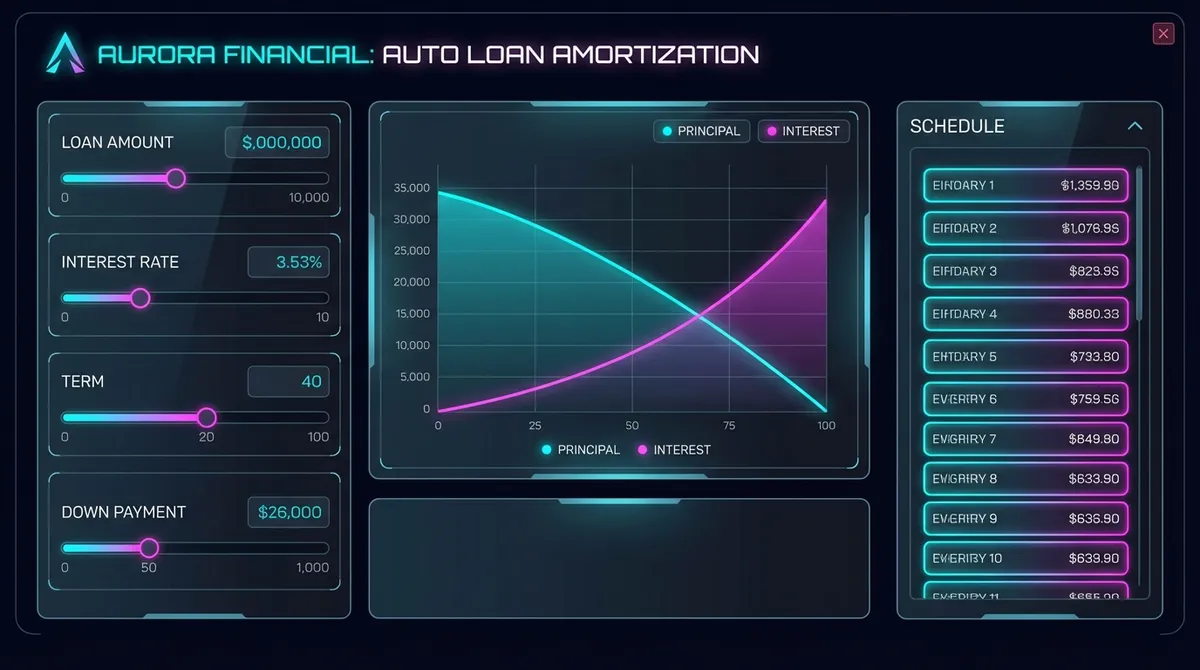

An auto loan amortization schedule is a comprehensive table that breaks down every payment you will make over the life of your loan. It shows exactly how much of your hard-earned money goes toward paying down the debt versus how much is lost to interest charges.

In the early months of your loan, a significant portion of your payment is eaten up by interest. This is because interest is calculated based on your outstanding balance, which is highest at the start. As you chip away at the principal, the interest charges decrease, and more of your payment goes toward the car's actual value.

Understanding this curve is critical for financial planning. It explains why you build equity slowly at first and why trading in a car too early often leads to "negative equity" (owing more than the car is worth). Our Auto Loan Amortization Calculator visualizes this financial journey, empowering you to make smarter decisions about your auto financing.

How to Use This Calculator

We designed this tool to be intuitive yet powerful. Here is a step-by-step guide to generating your personalized amortization schedule:

- Enter Loan Amount: Input the total amount you are borrowing. This should be the final price of the vehicle, including taxes and fees, minus any down payment or trade-in credit.

- Input Interest Rate (APR): Enter your Annual Percentage Rate. This figure is determined by your credit score and the lender's terms. If you haven't secured a loan yet, you can use an estimated rate based on current market averages.

- Select Loan Term: Choose how long you have to repay the loan. Common terms are 36, 48, 60, 72, or even 84 months. Remember, a longer term lowers your monthly payment but increases your total interest cost.

- Set Start Date: Select the date of your first payment. This ensures the schedule reflects the accurate timeline of your loan.

Once you enter these details, the calculator instantly updates to show your Monthly Payment, Total Interest Paid, and your estimated Payoff Date. Below the summary, you will find a detailed month-by-month table showing the breakdown of every penny you pay.

The Mechanics of Amortization

To truly master your auto loan, it helps to understand the math behind the scenes. Most car loans use a simple interest formula, but the amortization calculation ensures your payment stays flat.

The formula used to calculate your monthly payment is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ]

Where:

- M = Total monthly payment

- P = Principal loan amount

- i = Monthly interest rate (Annual rate divided by 12)

- n = Number of months required to repay the loan

While you don't need to memorize this formula, knowing it exists helps explain why a slightly lower interest rate or a shorter term can save you thousands of dollars. The "power" function in the formula means that interest compounds in a way that heavily favors the lender in the beginning.

For a deeper dive into how different variables affect your loan, try our Auto Loan Calculator to experiment with different scenarios.

Strategies to Pay Off Your Loan Faster

Seeing the total interest cost on an amortization schedule can be a shock. However, you are not stuck with that number. Here are proven strategies to accelerate your payoff and save money:

1. Make Principal-Only Payments

Most lenders allow you to make extra payments that go 100% toward the principal. By doing this, you reduce the balance that interest is calculated on for the next month. Even an extra $50 a month can shorten your loan by several months and save hundreds in interest.

2. The Round-Up Method

If your payment is $365, consider rounding it up to $400. It’s a small difference in your monthly budget, but over 60 months, that extra $35 adds up to $2,100 in principal reduction, plus the interest savings on that amount.

3. Bi-Weekly Payments

Instead of paying once a month, split your payment in half and pay every two weeks. Since there are 52 weeks in a year, you end up making 26 half-payments, which equals 13 full monthly payments. This "extra" payment each year drastically cuts down your amortization schedule.

4. Refinance for a Better Rate

If your credit score has improved since you bought the car, or if market rates have dropped, refinancing can be a game-changer. A lower interest rate flattens the amortization curve, meaning more of your payment goes to principal immediately. Check your potential savings with our Auto Refinance Calculator.

Amortization vs. Simple Interest

It is important to distinguish between the schedule (amortization) and the method (simple interest).

Simple Interest means interest accrues daily based on the balance. If you pay a few days early, you pay slightly less interest that month. If you pay late, you pay more interest, and less of your payment goes to principal.

Amortization is simply the plan that forces that simple interest calculation to fit into a predictable monthly payment. It ensures that by the end of the term, the balance is exactly zero.

Additional Resources

Financial literacy is key to making smart car buying decisions. We recommend consulting these government and non-profit resources for unbiased information on lending and debt management:

- Investor.gov: Amortization Definition- A clear definition and explanation of amortization from the U.S. Securities and Exchange Commission.

- Federal Trade Commission: Financing or Leasing a Car- A comprehensive guide to your rights and options when financing a vehicle.

Frequently Asked Questions (FAQ)

Can I change my amortization schedule?

You cannot change the original schedule without refinancing or modifying the loan terms with your lender. However, you can alter the effective schedule by making extra payments. Every extra dollar you pay shifts the schedule in your favor, shortening the term.

What is negative equity?

Negative equity, often called being "underwater" or "upside down," occurs when your loan balance is higher than the car's market value. This is very common in the first 1-2 years of an amortization schedule because the car depreciates faster than you are paying down the principal.

Does paying early help?

Yes! Since auto loans typically accrue interest daily, making your payment a few days before the due date reduces the interest charged for that period. Over the life of a loan, this habit can save you a noticeable amount of money.

Is it better to have a longer or shorter loan term?

Financially, a shorter term is always better because you pay less total interest and build equity faster. However, shorter terms come with higher monthly payments. You should choose the shortest term that still fits comfortably within your monthly budget.

How does a down payment affect amortization?

A larger down payment reduces the initial principal P in the formula. This lowers your monthly payment AND reduces the total interest paid. It also gives you a head start on equity, protecting you from being underwater on the loan.